Comprehensive Playbook on Startup Fundraising

How to fund your startup that aligns with your business goals from ideas to Series A

In the current fundraising environment, navigating traditional venture capital can be challenging and opaque, especially for many first-time tech founders.

For the founders reading this post, I want to provide a comprehensive guide on fundraising effectively that aligns with your startup’s business goals from ideas to Series A.

I will show you how to balance those two objectives while figuring out the following:

How much money do you need to raise to hit the following milestones?

How much dilution should you be comfortable with for each funding round?

Dilution refers to the part of the company you give to investors in exchange for their investment in your company’s equity.

In the following posts, I will provide other distinct fundraising methods, including bootstrapping and applying for accelerators such as Y Combinator, that you can consider.

Roadmap

First, we will use the following Product-Market Fit (“PMF”) guide as our roadmap to help us identify our business goals and structure fundraising accordingly.

Note that many builders’ actual product development experience is often less linear than the above guide shows.

Nevertheless, this guide provides an excellent exercise on how to align fundraising with business goals.

Let’s assume we are first-time founders with a limited network trying to figure out how to launch a B2B enterprise software company. Here is the snapshot of our fundraising roadmap.

Idea Phase

In the first phase, the primary goal for anyone considering starting a company is to validate the Market Opportunity by understanding your customer’s problem.

“Around 35% of startups fail because there is no need for their product in the market.” - Problem Validation And Customer Discovery Interviews.

In the pre-launch stage, we first prioritize understanding our customer’s problems through customer discovery interviews. Before quitting our job to start this company, we should validate the customers’ key pain points. You can read more about this here.

Since customer conversations require only slides, questionnaires, and time commitment, there is no need to start a company and do any fundraising officially.

Concept Phase

In the concept phase, our business goals are to prioritize the key customers’ problems from the customer discovery interviews and ideate/design a solution.

Since this phase requires an early product design ranging from initial mockups to prototypes, we can raise a small amount of money to undertake this project.

At this point, we can also consider officially starting the company (at least part-time).

Here are some key considerations:

Can we do the early product design ourselves or hire/outsource a UI/UX designer/engineer?

Can we use our money to fund all the ongoing costs (bootstrap)?

If the answer is “no,” we need a $100,000 budget to cover the initial cost, with additional reserve for iterations. We can consider the following:

Register the company using Stripe Atlas and get a business account with neo-banks such as Mercury. Given the recent banking crisis with SVB and First Republic Bank, you should do additional due diligence on finding the right banking partner for your startup.

Raise $100K in the Friends & Family round, including any angel investor from your network. I will use Simple Agreement for Future Equity (SAFEs) as the main instrument for early-stage fundraising. Here is the SAFE document template.

Using SAFE saves us $25-50K of legal fees usually associated with issuing equity.

Since the startup is still in the idea/concept phase, let’s set the price at a “generous” $3M post-money valuation.

Let’s assume our company starts with an initial 10,000,000 common shares. We also created an option pool for employees, advisors, and consultants throughout the company's life.

Here is our pro forma cap table at inception.

Don’t forget that SAFE investors are not on the cap table until the SAFE investments convert at the following priced round (ex: Series A).

Here is a separate table for us to keep track of any potential dilution. After the friends & family round, we estimate that our founders' ownership is around 89.2% by subtracting the SAFE dilution and option pool.

At this moment, we will start planning our future fundraising by building our investor network in the following buckets:

Angel investors from operators/investors like myself and my friends at Hustle Fund Angel Squad.

Micro VC/small funds ($10M or less fund size) & syndicates like PaperJet Ventures.

Institutional VC/seed fund.

Committing Phase

After iterating our product concept, our next goal is to launch its beta version to target early adopters. At the same, it’s time to make our first hires, especially for the engineering and design teams, depending on needs.

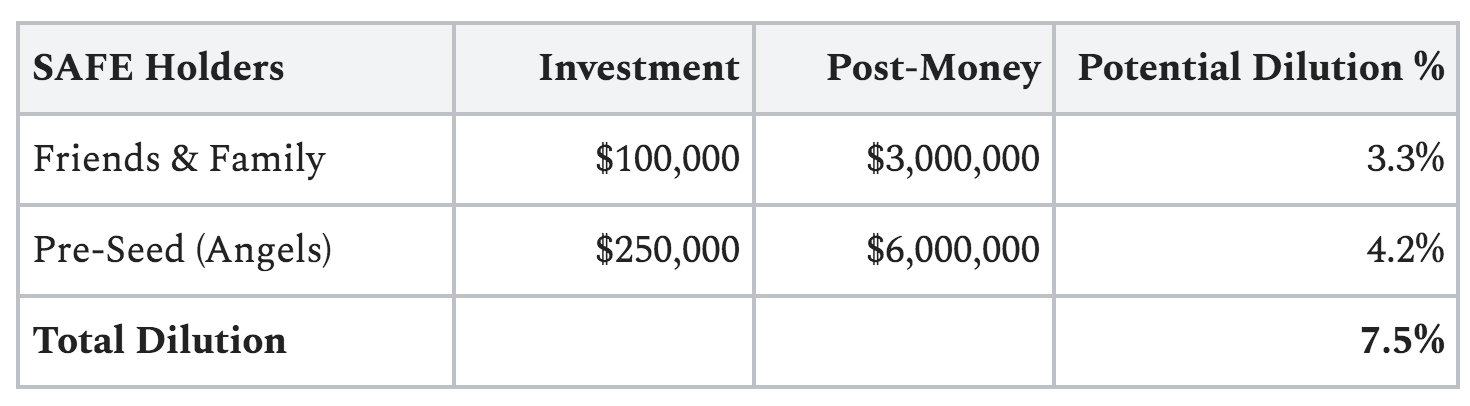

We will raise a $250K pre-seed round for this phase at a $6 million post-money valuation. This budget assumes we are operating very lean by forgoing any founders’ salary and going fully remote.

We primarily target value-added angel investors for the first fundraising and are open to accepting checks as small as $5K. While the checks are small, early angels can add value through introductions to their network of other angels and connections with institutional VCs who could be in your cap table as you progress.

In Freshpaint’s insightful post, angels’ value-adds illustrate how any unnamed angel investor’s $5K check was responsible for over 50% of its seed round.

Value-add angels/operators are very helpful in the early days, ranging from providing warm intros to other investors and sharing expertise in crucial areas such as product design and GTM to providing reputation signals.

We will build a pitch deck based on our founders/market fit narrative, market size, and highlights of our current learnings and tractions.

The table below shows the potential SAFE dilution after the pre-seed round. We estimate that our founders' ownership is around 85.0%.

Validating Phase

In this phase, our goals are to launch product version 1.0 and show our product is working with key metrics that can set us up for Series A funding.

What You Should Expect

In this phase, startups spend more time experimenting (sometimes pivoting from initial ideas) before things start to work. There is a high default dead risk as founders often underestimate the time to build and find PMF and realize that their companies need more capital than initially estimated.

High Hurdle to Series A

In the current fundraising climate, there is a high hurdle for B2B enterprise software startups raising Series A. I asked an experienced early-stage VC to provide the following valuable insights.

“Vertical/sector matters a lot. I have portfolio companies with less than $1M ARR that were able to raise Series A because it’s GenAI. Some companies at $2.5M+ ARR are capable as well.

On the other hand, some companies with $2M+ ARR struggle to raise this round given their market and vertical. Growth rates matter also.”

For this exercise, we must hit around $1.5-2M ARR with 50-100% year-over-year growth and consistent retention metrics.

Next, we must consider that our team will need various sales, partnerships, and marketing channels to acquire enough customers to hit the key metrics. Given this requirement, we must grow our product, design, engineering team, and early hirings in other areas, especially customer support/service, to anticipate incoming customers.

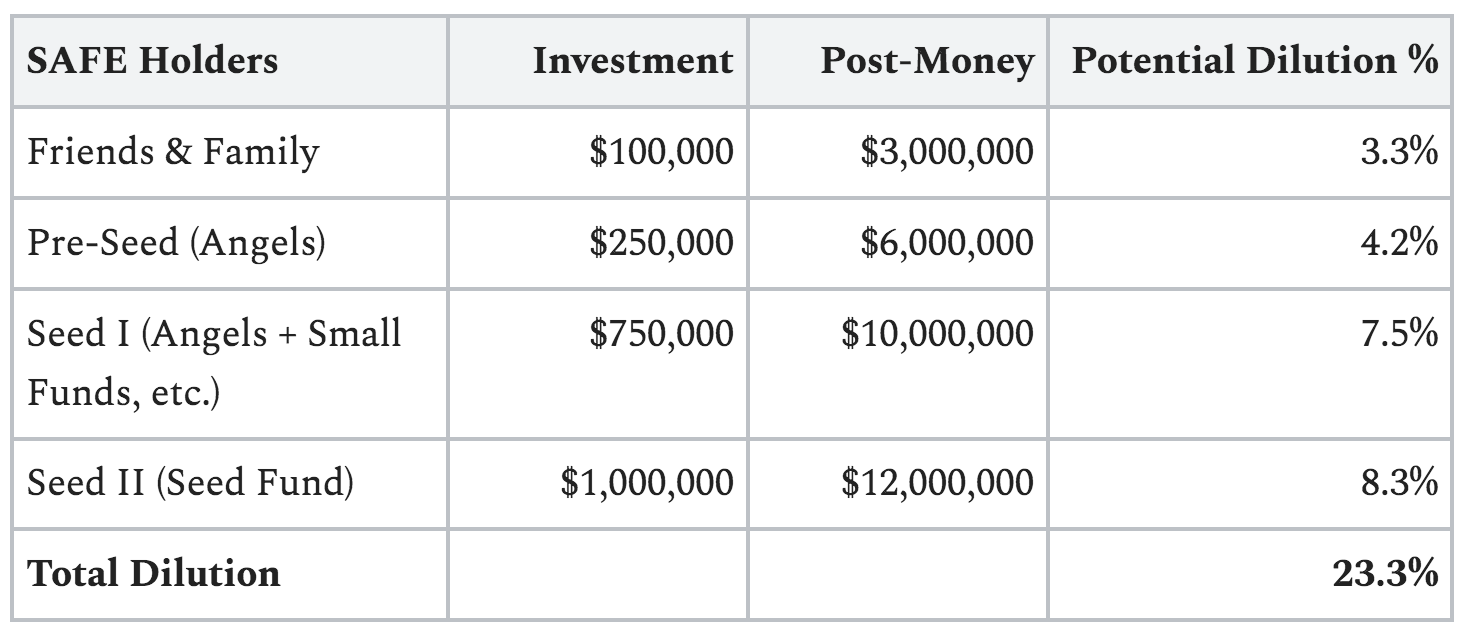

We will raise a $1.75 million seed round based on the above budget plus office-related costs. It also requires us to plan for an 18-24 months runway toward Series A. If you need help calculating the runway for your startup, read this guide from Brex.

Raising a seed round also means founders can finally compensate themselves. According to this guide, a founder's salary is typically 50K at Pre-Seed, 100K at Seed, and 150K at Series A.

Given the size of the round, I recommend raising it in 2 tranches:

By first reaching out to angel investors and small funds/syndicates for Seed I, we can close the funding faster and use the funds to build the product and momentum.

Raising from institutional venture funds takes longer than anticipated, a critical risk for many early-stage startups struggling with capital.

Raising in increments also helps us to be disciplined with costs and avoid over-hiring.

We can start to reach VC firms as soon as we hit some momentum in Seed I fundraising or some inflection in our product development and sales.

The table below shows the potential SAFE dilution after the two tranches of the seed round. We estimate that our founders' ownership is around 69.2%.

Scaling Phase

In the last phase (for this exercise), we aim to scale our sales to early adopters with a repeatable sales process and transition towards building the company.

A repeatable sales process means we have a proven sales playbook that can identify primary users, decision-makers, buyers, and influencers. We have successfully fine-tuned our product, pricing, and messaging. We are close to PMF or about to hit it during this phase.

Achieving this milestone also allows us to gradually transition from founders-led sales to handling all the GTM and sales activities to a sales team we need to build. In addition, this company-building step will shift our attention towards expanding our products or services into new markets.

We will raise $10 million of Series A at a $40M post-money valuation. Series A's usual range of dilution is around 15-25%.

Given the market uncertainty affecting Series B, it’s prudent to plan Series A to account for an additional runway of up to 24 months to prepare for possible prolonged fundraising in the following Series B round in exchange for giving up 25% dilution ($10M round/$40M post).

Here is what our cap table looks like after Series A. I will share how priced round conversion works in the next post.

Play the Long Game

For any founder who thinks about optimizing for high ownership and valuation after looking at this example, I advise them to take a long view of their companies.

Startups’ valuations, driven by supply and demand, depend on many factors, including stages, sector, macroeconomic (interest), competition, and relative comps.

Instead of over-optimizing your fundraising structure by targeting the lowest dilution for each round, here are my advice:

Raise quickly on fair pricing with the right investors on the cap table so you can get back to the business of building the product/company.

There is less pressure to grow to justify any inflated valuation.

Missing key milestones, especially during a market downturn, can lead to down rounds with investors asking for more control.

When investors have control, they could replace you with external CEO if the company’s growth is below expectations.

When it comes to fundraising, you should always align with business goals first. Once you execute, you will be in a stronger position to control your destiny and optimize for the best terms in the future.

Final Note

For founders working on exciting problems, check out my Investment Thesis 1.0.

If you want to learn more or have more questions, please get in touch with me on Twitter.

Thanks to Jen Liao and Jaireh Tecarro for providing valuable insights and reading drafts of this post.

PS: Sign up☟ if you find this interesting. Email me if you have any excellent topics for me to explore more!

If you liked this post from Ante Up Newsletter, why not share it?

Chris Kong, great post! For founders with some prior work experience in the Idea, Concept, or Committing phase, check out FFL Startup Accelerator to join an amazing community of other experienced professionals aspiring to start a tech startup: https://www.joinffl.com/