Designing an Advanced Manufacturing Strategy for the AI Era

Why “Industrial AI” needs policy, industry, and venture to align

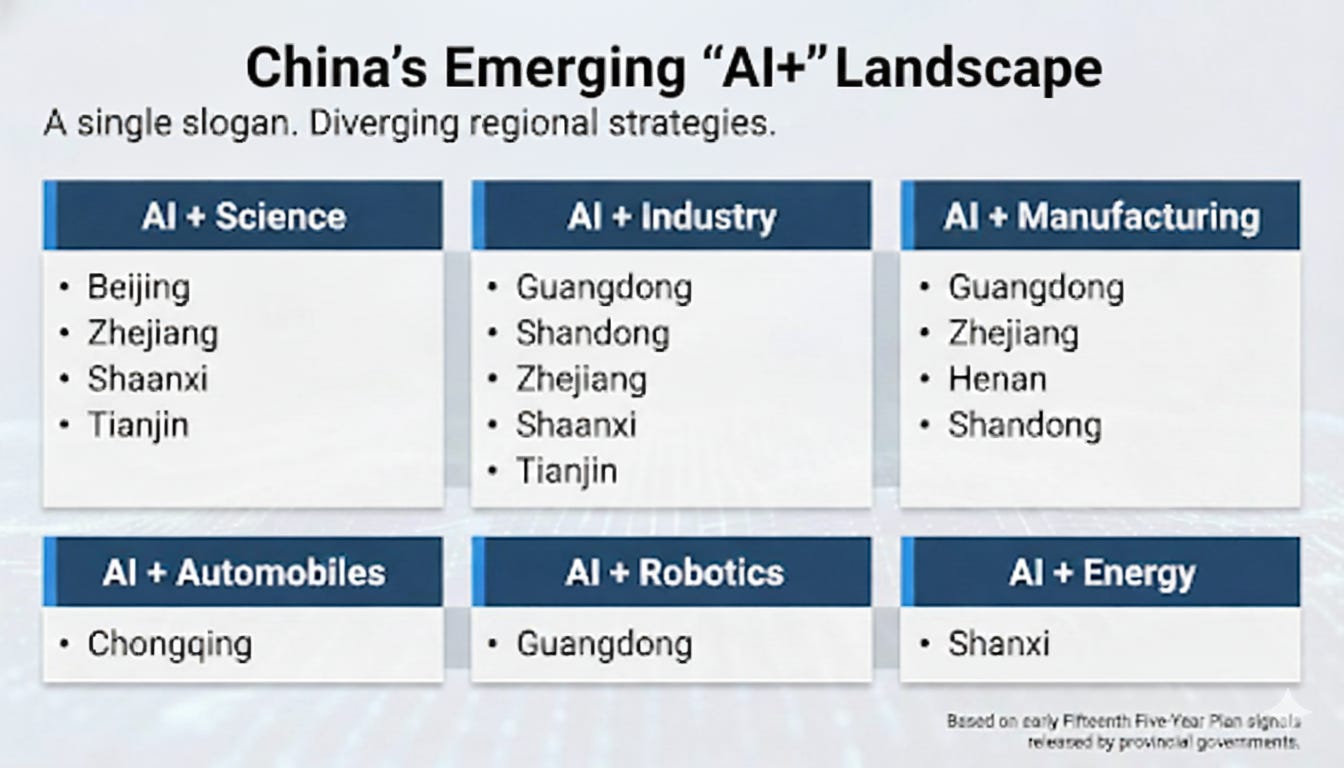

China’s early Fifteenth Five-Year Plan signals a shift in how the country treats Industrial AI. It is not an optional innovation add-on, but foundational infrastructure woven into broader industrial modernization and “AI Plus” integration across production systems.

That framing changes how factories get built. AI requirements now show up in plant layouts, supplier contracts, and provincial funding targets before a single machine is ordered.

A few years ago, the debate was whether AI belonged on the factory floor. Today, the real problem is that factories struggle without it. Across multiple provinces, “AI+” is not a software push. It shows up as specific mandates to replace legacy machines, standardize data interfaces, and align suppliers around shared production targets.

On paper, it is one slogan. On the ground, it turns into very different execution paths.

So here’s the real question for the U.S.:

If China is building robotics as infrastructure, why does the U.S. still treat it like a pilot?

This isn’t a standoff. It’s a race between two manufacturing systems built on different assumptions.

A recent Stanford US–China dialogue framed it as strategic competition without escalation.

China designs programs around deployment from the start. In the U.S., most funding still stops at pilots that never become production systems.

Even in Washington, this framing is starting to surface. After a six-year pause, the Congressional Robotics Caucus was recently relaunched around a blunt premise: reshoring without robotics and workforce alignment is a dead end.

It’s not a solution. But it’s a signal that the problem is no longer invisible.

People inside factories have been living with this disconnect for years. The policy world is only now catching up.

We’ve spent years debating reshoring and industrial policy. Agencies like the Department of War (“DoW”) and Department of Energy (“DoE”) are trying to lead the charge.

But we may still be missing the point:

What if advanced manufacturing is not a support function at all, but something closer to power generation or national security? Something you plan around, not bolt on later.

Below, I’ll walk through the core breakdowns holding back U.S. Industrial AI, then outline a deployable playbook for capital, policy, and talent to realign.

Without production systems that can actually absorb new technology, the U.S. will continue to invent things it struggles to manufacture at scale.

The Strategic Gap: Innovation Without Alignment

The U.S. leads the world in AI software.

That success came from decades of compounding advantages.

Deep university research

A global magnet for talent

Open-source culture

And relentless private investment from NVIDIA, Meta, Amazon, and Google

But in Industrial AI, where intelligence is embedded into manufacturing, robotics, and energy systems, we lag.

As one factory operator recently put it:

“World-class robots, paper workflows, siloed data, and still no way for factories to learn from each other.”

Not because we lack innovation, but because we lack alignment.

These failures show up on factory floors every week. Here is what they look like in practice.

1) Fragmented Funding

Research funding lurches every time the federal budget shifts.

The standard 10-year venture clock is built for software, not for factories that take years to stand up.

Only a few companies ever receive compounding capital. Most industrial startups stall long before scale is even in sight.

Tesla looks like a miracle story until you trace the inputs. Years of government support, aligned policy, and patient capital gave it time to learn how to build before anyone demanded scale. Most industrial startups are pushed to prove economics long before their systems are ready.

2) Pilots Instead of Deployments

Pilots create demos, not ecosystems. Without deployment density:

Suppliers don’t learn

Cost curves don’t fall

ROI never materializes

Systems never compound

In practice, this phase breaks down because each deployment becomes a bespoke rebuild. Knowledge, telemetry, and lessons don’t carry forward.

That’s where most pilots die.

We’ve already seen this failure mode at scale.

After the bipartisan infrastructure bill unlocked funding, transformer lead times stretched from roughly 20 months to as long as five years, not because capital was missing, but because skilled labor and deployment capacity could not scale fast enough, as noted by Heather Carroll of Path Robotics.

The checks showed up after the bottlenecks were already baked in.

The factories were not ready for the money.

You can see the fallout on factory floors today.

Across U.S. manufacturing plants, world-class robots coexist with paper checklists and whiteboards. ERP systems are decades old, data is siloed, and Excel remains the default interface. AI is discussed everywhere, but deployed almost nowhere. Even factories owned by the same company operate like separate worlds.

These observations reflect firsthand reporting by Harmony’s founder, George Mungui, who visited more than a dozen U.S. factories and documented the same pattern: advanced hardware constrained by fragmented software, aging systems, and missing integration.

3) No Anchor Demand

Anchor demand is when a buyer shows up for five years, not five pilots. That is when suppliers stop hedging and start building real capacity.

Without predictable, multi-year demand:

Suppliers won’t expand capacity

Investors won’t underwrite early infrastructure

Startups optimize for survival, not scale

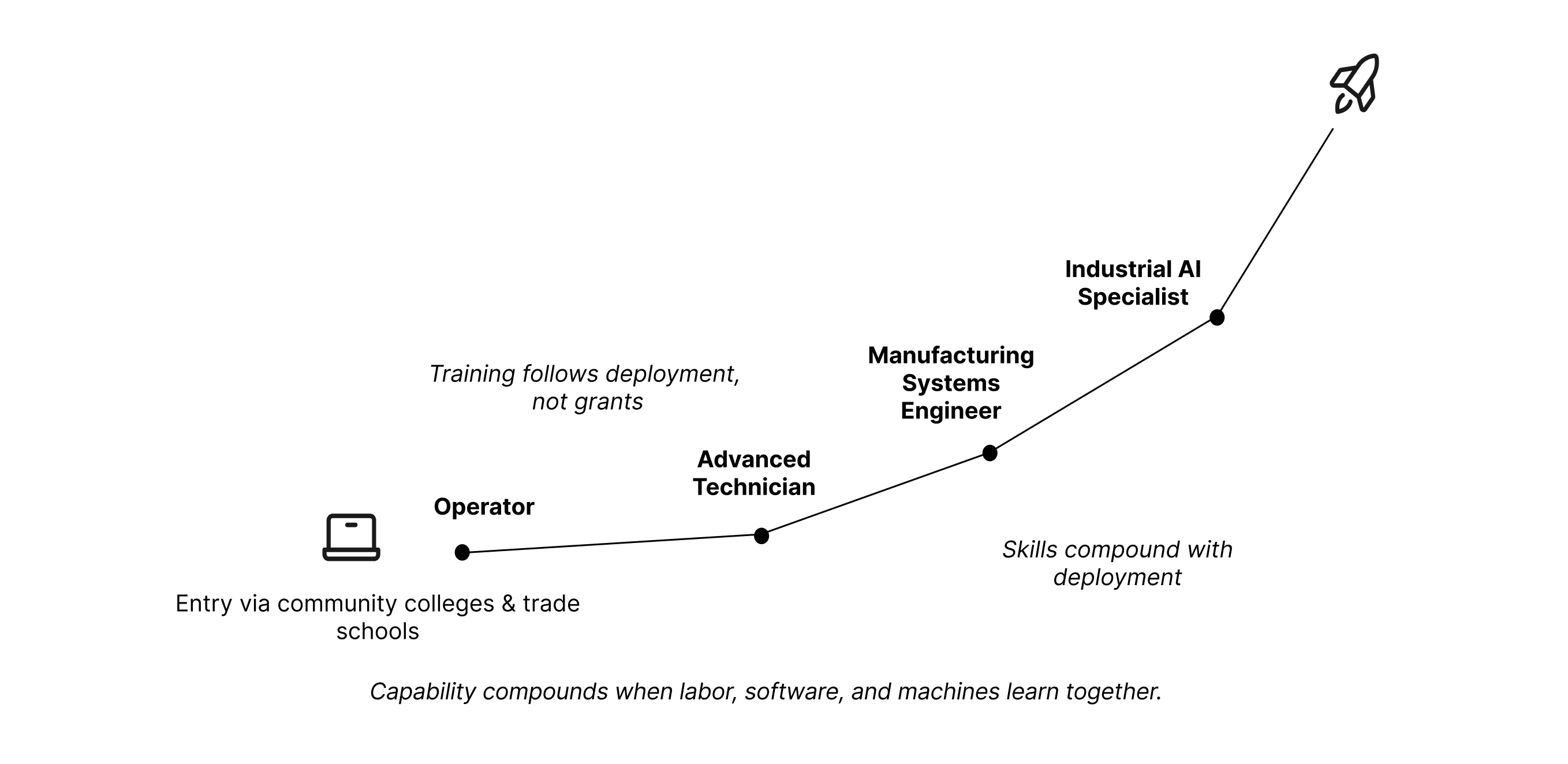

4) Broken Talent Ladder

The U.S. celebrates two extremes: elite software roles and traditional trades.

Industrial AI requires the ladder in between:

operators → technicians → systems engineers → Industrial AI specialists.

The missing link is the middle of the ladder: technicians and systems engineers who can operate, maintain, and improve intelligent machines in real environments.

Only about one in ten machine learning engineers work on robotics, even though robotics is where AI turns into physical capability, as Ashish Kapoor, co-founder of General Robotics, has noted.

The hardware is here. The people who know how to run it, fix it, and improve it are not.

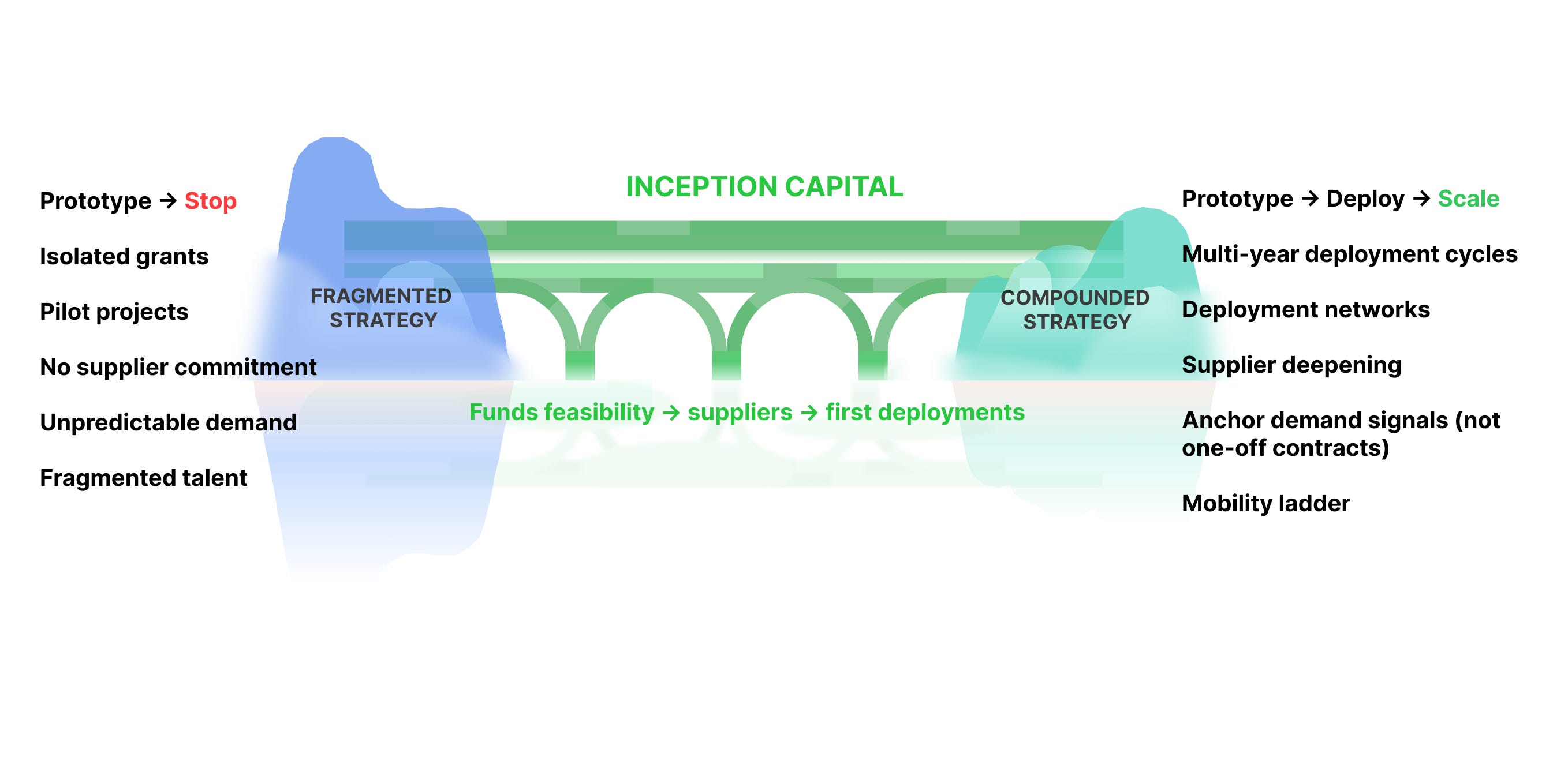

Fragmented Funding: Why Inception Capital Is Missing

A few specialist firms will write the first check. Most of the venture model is not built for the first two years of Industrial AI.

Before any factory can scale, founders run into the same four problems.

Technical feasibility. Can this system actually hit real cycle times under real constraints?

Supplier reality. Who will build the first parts, and at what minimum order size?

Deployment economics. How does it perform in the field, not in a lab?

Dual-use paths. Can early DoW or DoE demand coexist with commercial buyers?

Most funds still evaluate Industrial AI as if it were software. That shows up in three ways:

small exploratory checks

traction-first expectations

wait-and-see posture

Industrial AI is not SaaS.

It needs investors who fund proof in the real world, not prettier pitch decks.

This is where the system breaks.

Without inception capital, policy floats in the abstract, and suppliers stay on the sidelines.

Everyone waits. Nothing compounds.

What Inception Capital Actually Changes

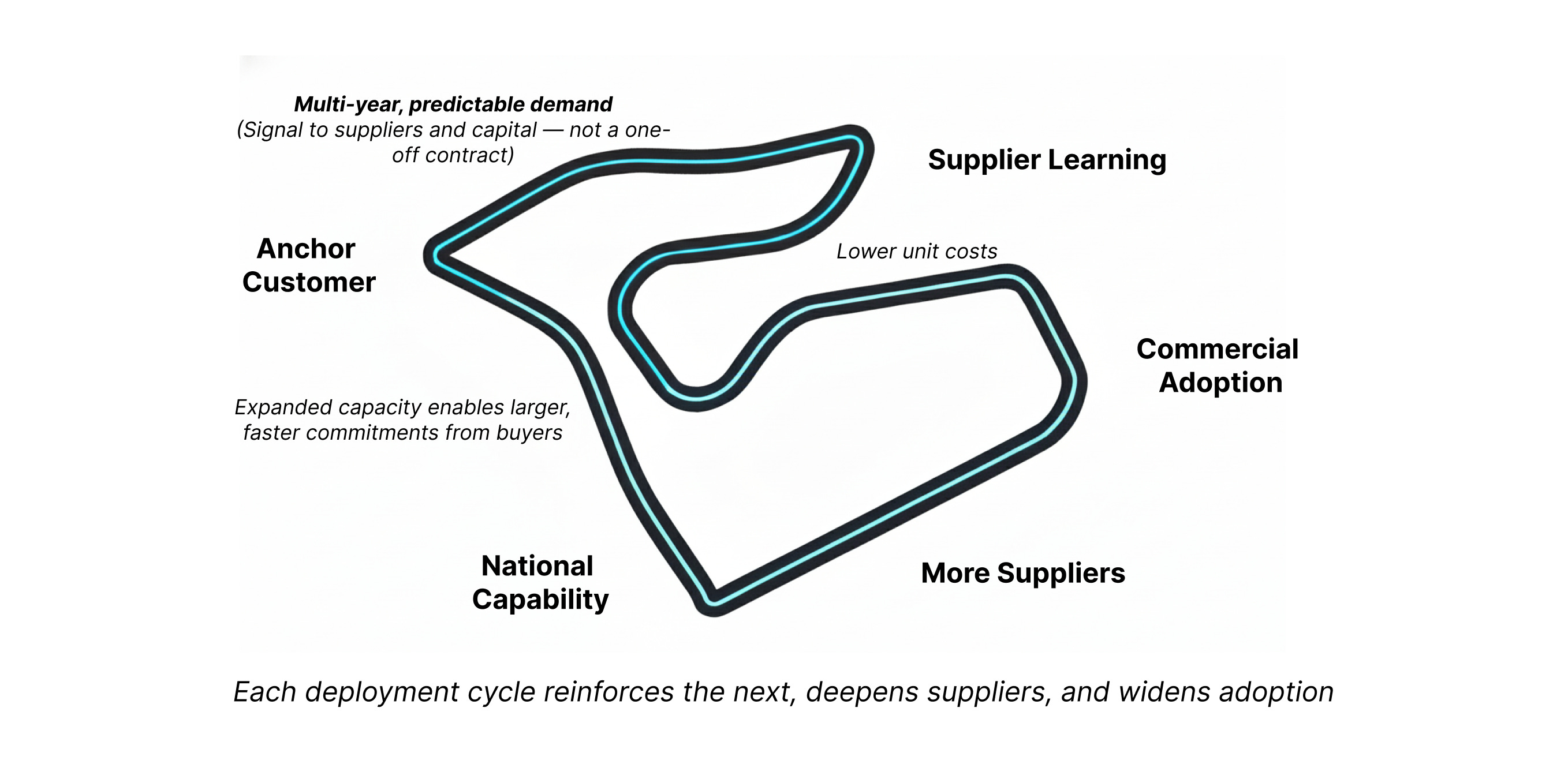

Manufacturing Needs an Anchor Customer

If the U.S. wants manufacturing to compound the way software did in Silicon Valley or hardware did in Shenzhen, one problem has to be solved first.

Industrial AI does not grow from “fund and walk away” pilots. It requires sustained ownership of deployment so systems can learn and improve in real production environments.

China’s advantage is not cheap labor. It is long-cycle demand.

Ten- to twenty-year roadmaps cascade from Beijing to the provinces.

Each deployment teaches suppliers, builds workforce capability, lowers costs, and makes the next rollout easier.

Meanwhile, the U.S. runs pilots that never scale.

We stop right when the learning curve should begin.

Each pilot uses different interfaces, data formats, and operating assumptions.

Suppliers learn once, then relearn the same lessons again.

Provisions in the latest National Defense Authorization Act (“NDAA”) point toward multi-year procurement and production capacity, not just R&D or one-off prototypes. The direction is right, but the approach is still fragmented.

It does not have to work this way.

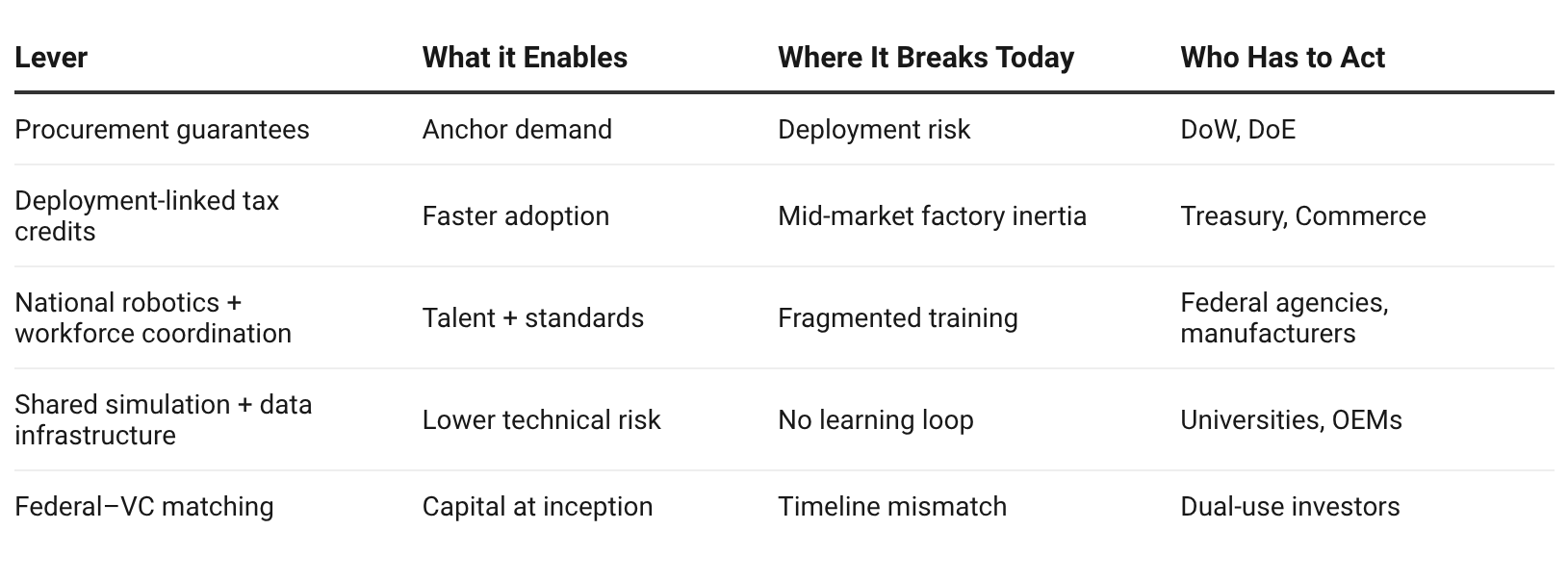

If the U.S. is serious about reindustrialization, the public sector has to act as an anchor customer.

China does not rely on a single anchor customer in the way the U.S. might. Instead, central plans set direction, and provinces, state-owned enterprises, and large industrial buyers execute against shared multi-year targets. The result is coordinated demand at scale, even without a single buyer signing every contract.

DoW and DoE already have the budgets and the mandate. If they show up with predictable demand instead of one-off grants, suppliers will scale. Cost curves fall. The same batteries, motors, sensors, and chips then serve both government and commercial buyers.

Capability Compounds Over Deployment Cycles

A practical starting point is simple. Long-term procurement. Small factory clusters. Clear dual-use targets.

Anchor customers are not just buyers. They tell suppliers, founders, and investors when it is safe to commit.

Some of this thinking is starting to show up in policy. The 2026 NDAA includes multi-year purchase commitments and direct funding for production capacity. That is what lets suppliers invest before the next contract arrives.

DoW will never be the main buyer for most of this tech. But its early commitments can carry suppliers through the hardest years.

Without predictable demand, suppliers stay on the sidelines, founders burn out, and every pilot turns into a reset.

The Microfactory Strategy

The U.S. keeps announcing megafactory and gigafactory plans. EVs. Defense. The list keeps growing.

But megafactories drag a lot with them.

Capital up front.

Years of construction.

Politics, unions, permitting.

Supply chains that snap when anything goes wrong.

Only a handful of companies can actually make this work.

The real constraint is not engineering. It is depreciation. Factories built twenty years ago are still on the books, and nobody wants to torch them before they are written down.

Incumbents are locked into factories designed decades ago. Rebuilding production systems before existing assets are fully written down destroys capital, so boards resist even when better automation exists. The result is structural inertia. The biggest winners won’t be retrofitting old plants. They’ll be the ones designing new products and production systems from scratch.

This is the moment where paths split.

China can pull capital, labor, and suppliers into a few mega-sites and plan ten years out.

The U.S. cannot. Talent sits in universities and labs. Demand is scattered across defense, energy, and commercial buyers.

That fragmentation is not accidental. It is the system we inherited.

Microfactories exist because the U.S. does not build like China. They are what happens when you design around fragmentation instead of trying to fight it.

So what does this look like on a real factory floor?

You can already see early versions of this. Fewer people on the floor. More machines that need supervision instead of babysitting.

The closest thing we have today is China’s “dark factories.” They run 24/7 on AI, robotics, and dense sensing, inside a system the U.S. does not share.

It works in pockets today. What is missing is the ability to copy it, site to site, without starting from zero.

From Concept to Execution: Software-Coordinated Microfactories

America does not win with giant plants. It wins by placing small, fast factories near:

university and technical talent

simulation ecosystems

supplier, and OEM clusters

DoW and DoE infrastructure

Think of microfactories as production nodes you can spin up quickly and reconfigure in software.

The model we want to see:

The model starts with DoW or DoE as the anchor, paired with at least one commercial buyer. That combination gives suppliers confidence to commit. Once that happens, deployments stop being isolated, and demand stops resetting.

What Microfactories Enable

Design, build, test.

Then do it again next week, not next year. Short cycles turn into more shots on goal.

This is the closest the U.S. gets to Shenzhen-style compounding today.Local supply chains

Post-COVID fragility + tariff uncertainty expose long-haul suppliers.

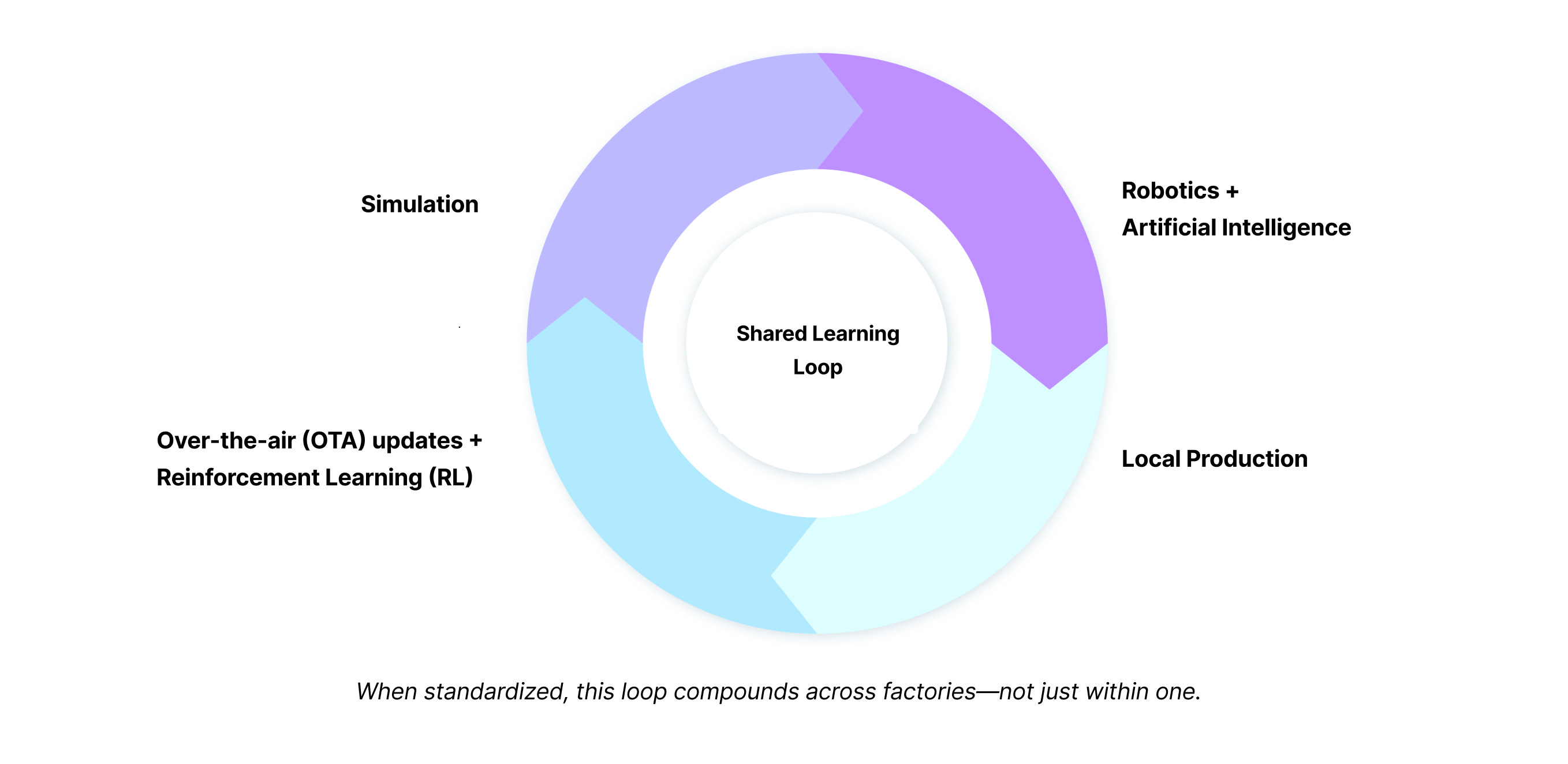

Microfactories + local suppliers solve “wait 14 weeks for a part.”Reinforcement learning for factories

With sensing and OTA updates, production starts to look like a feedback system instead of a fixed process.

Microfactory’s Data Flywheel

Factories as a Platform

To build a “Shenzhen of the West,” microfactories must be modular, extensible, and open:

plug-in modules (“factories in a box”)

shared testing + metrology

shared supplier networks

standardized automation cells

If factories cannot update, adapt, and share improvements, they freeze in place while China keeps pulling ahead.

Manufacturing as Dual-Use Capability (Energy + Defense)

When DoW commits to the same system for five years, suppliers stop guessing. They start hiring, buying tooling, and locking in vendors instead of waiting for the next Request for Proposal (RFP).

To make this real, three shifts must happen:

1) Fund Industrial AI + Digital-Twin Simulation

Industrial AI depends on simulation, not static design files, but continuously updated operational models.

A digital twin is a living model of a factory that changes every time the real line changes.

If a robot drifts out of tolerance, the model drifts with it.

If a weld fails at 2 a.m., the twin records the conditions that caused it.

Most factories only learn that something is broken after bad parts are already on a truck.

Teams use digital twins to test changes without stopping production, catch failures before they become scrap, and train systems before expensive mistakes happen.

This simulation layer supports modeling, quality assurance, autonomous systems testing, and process optimization.

Today, these layers are underfunded, even though they are required for Industrial AI to scale.

2) Build Shared Digital-Twin Data Architecture

Today’s fragmentation prevents learning.

No shared telemetry means no shared improvement curve.

Policy already recognizes part of this problem on the qualification side. The NDAA emphasizes standardized specifications, expedited qualification, and third-party certification to reduce friction across programs.

Qualification reduces friction, but it does not create learning loops across deployments.

Funding helps. Procurement helps. But the people running the machines still cannot move what they learn from one site to the next.

In the field, teams report the same pattern. Every deployment becomes a bespoke rebuild.

Telemetry does not transfer. Interfaces do not align. Benchmarks do not persist.

Without shared data, factories cannot learn from themselves or from each other.

A shared digital-twin and telemetry layer would do a few very unglamorous things that almost nobody is funding today:

Align vendors around common interfaces

Accelerate dual-use startups

Enable benchmarking across factories and systems

Turn every deployment into a learning loop

Standardization is what lets one good idea show up in the next factory instead of dying inside the last one.

3) Treat Manufacturing as Infrastructure

Procurement stops when the contract is signed. Infrastructure only begins when the system survives its first year in the field.

Manufacturing needs to move past one-off contracts and into systems that get better every time they run, including:

continuous improvement, not one-time awards

predictable, multi-year demand

shared supplier networks

platform-style deployment cycles

The language exists in Washington. On the factory floor, almost nothing feels different.

The NDAA frames manufacturing across funding, qualification, workforce, networks, and policy. This is a clear signal that capacity is no longer viewed as a one-off procurement problem, but as an ecosystem that must be sustained and upgraded over time.

What nobody has figured out is how to make this survive beyond the pilot.

Think F1, Not Waterfall

When simulation, data, and infrastructure align, industrial AI starts to look like an F1 pit crew:

Speed does not matter if every plant is rediscovering the same failure in isolation.

Telemetry, role clarity, and repeatable execution turn each cycle into usable learning.

This is the operating model the U.S. needs across energy, defense, and manufacturing. One system that gets better every lap.

Talent: AI Should Augment, Not Replace

Automation is usually framed as job loss.

The real pressure is demographic.

Roughly 157,000 skilled tradespeople, including welders, are approaching retirement, while nearly 80% of critical industrial work remains manual. If that knowledge isn’t captured and scaled through real deployments, it disappears. Automation isn’t about replacing workers. It is the only way to compound expertise before it’s lost.

The problem isn’t unemployment. It’s that there are no clear paths into the jobs that already exist.

Three realities we must accept:

As experienced workers retire, their knowledge is lost instead of being passed on and compounded.

Without shared systems, every shift change becomes a reset. Teams relearn the same fixes on different lines, in different buildings, every week.

Much of the world’s tacit manufacturing expertise lives in Japan, Korea, Taiwan, and other advanced manufacturing economies. Rebuilding U.S. capability will require deep partnership, not isolation.

The Real Shift: Old Jobs Disappear, New Jobs Don’t Have Pathways

High-value roles emerging now include:

Teleoperation: remotely monitoring and intervening in automated systems.

Simulation and digital-twin supervision: testing and improving systems in software before deploying changes.

Maintenance and AI diagnostics: combining hands-on repair with predictive software tools.

Systems engineering for Industrial AI: integrating machines and software into reliable production systems.

Learning While Producing: Paid upskilling through real factory systems

These roles aren’t abstract titles. They are the natural progression when training is embedded in live factory systems.

The U.S. Needs a New Workforce Blueprint

Today’s workforce programs live far from the factory floor. Skills are taught in classrooms. Production happens somewhere else.

That separation is why nothing sticks.

Training has to live inside real deployments:

microfactories

robotics rollouts

dual-use hubs

simulation centers

Here is the part most people miss. The funding model already exists.

A technician who keeps a robotic cell running is cheaper than downtime. That is why operators pay.

Every trained worker shortens rollout cycles across a supplier network. Anchor customers feel that pain first, so they co-fund.

Public programs only work when training lives on live systems, not in empty labs.

This is how production gets financed. Training has to follow the same logic.

A Modern Night-School Model

This is not a new idea. During past industrial transitions, many engineers retrained at night while working full-time jobs to support their families, including immigrant engineers during the semiconductor boom.

Most recently, workers from nontraditional backgrounds have done the same, attending night and weekend programs to move into software roles while continuing to earn a living.

We need:

night-school programs inside community colleges

colocated with deployment sites

co-designed with DoW, DoE, OEMs, and startups

focused on high-value Industrial AI roles

Training must follow deployments, not precede them.

Bottom Line

Jobs rarely vanish in a single layoff. What changes first is who understands the machines.

When only a handful of people know how a line actually behaves, production slows the moment one of them walks out.

Align training with deployment, and that risk compounds in your favor.

Summary: Policy and Venture Have to Move Together

If Industrial AI is going to scale in the U.S., policy and capital have to operate on the same clock.

Today, they move on different clocks. That’s why the table below feels more like a repair manual than a strategy slide.

Questions That Actually Matter

What would a U.S. microfactory cluster look like if it were designed on purpose?

Should advanced manufacturing be treated as national infrastructure, the way we treat energy or broadband?

Which agencies can act as anchor customers today? DoW, DoE, NASA, or some combination?

How do we co-fund early Industrial AI platforms so government demand and venture capital reinforce each other instead of drifting apart?

These decisions determine whether factories learn across cycles or whether every new program resets back to zero.

Closing

Thanks for reading this far.

The future of industry won’t be built inside a single factory.

When capital, policy, data, deployment, and talent move on different timelines, nothing compounds. Systems reset instead of improving.

When those layers finally line up, Industrial AI stops feeling like a project and starts behaving like a team that learns every lap. The question is how many cycles we burn before that happens.

Best,

Chris Kong

Founder & GP, PaperJet Ventures

P.S. A heartfelt thank-you to Bola Adegbulu, Ellen Chang, Jen Liao, and Jaireh Tecarro for their invaluable feedback, thoughtful tips, and unwavering support in shaping this piece.