Under-Automated, Overlooked

Why Robotics Keeps Missing the Manufacturing Capital Cycle

This isn’t an essay about whether robots work. Most of them do.

It’s about what happens after the demo, when capital has to live with the system.

If you allocate capital, sit on boards, shape policy, or back companies operating in physical systems, this is a look at where operational ownership and capital underwriting actually break — and what it takes for robotics to compound instead of stalling.

What this essay argues

∙ U.S. robotics isn’t failing on technology. It’s failing on how systems are underwritten once robots leave the demo floor.

∙ Factories don’t buy robots. They underwrite systems that have to survive depreciation cycles.

∙ Most deployments stall after installation because ownership and learning don’t carry forward.

∙ Capital compounds only where failure is owned, recovery is priced, and repeat deployment is possible.

∙ The next robotics wave comes from balance-sheet environments, not demo floors.The Illusion of Robotics Leadership

America builds some of the most recognizable robots in the world.

Optimus.

Figure.

Atlas.

They dominate headlines, conference stages, and keynote reels. If you follow robotics through press coverage, it’s easy to assume the U.S. is far ahead.

Spend a week inside real factories, and that assumption starts to fall apart.

The United States runs just under 300 robots for every 10,000 manufacturing workers. South Korea runs more than 1,000. China sits near 470. Even smaller industrial economies deploy automation more deeply than we do.

Density alone doesn’t explain the gap.

China now consumes roughly a third of the world’s industrial robots each year. The U.S. accounts for less than ten percent. The difference isn’t ambition. It is absorption capacity, shaped by who can actually deploy systems, keep them running, and justify the next install after the first one drifts.

The more revealing signal isn’t the ranking. It’s where the robots actually end up once you stop looking at press releases.

Roughly 40 percent of U.S. industrial robots are deployed inside automotive plants. Another 20 percent are tied up in electronics and heavy machinery. Most of American manufacturing barely touches them.

As Formic’s founder, Saman Farid, puts it:

“Most robots in the U.S. are deployed in automotive and logistics, which make up less than 2 percent of the country’s manufacturing labor. That means 98 percent of U.S. factories still operate with little to no robotics support.”

The technology works. The demos usually do too.

What breaks is everything around deployment. How robots are sold. How factories underwrite them. Who owns performance after the install team leaves.

When something drifts at 3 a.m., learning doesn’t compound. It resets. Downtime stops being a technical issue and starts showing up as a balance-sheet problem.

That’s the gap most U.S. factories live in. Approval happens upstairs. Failure shows up on the floor.

The Overlooked Majority Becomes the Binding Constraint

When people talk about U.S. manufacturing, they usually picture defense primes, automakers, or semiconductor fabs. Those companies dominate headlines, site visits, and policy decks.

They are not the industrial base.

The U.S. has more than 239,000 manufacturing firms. Fewer than 4,200 companies employ over 500 people (source: National Association of Manufacturers). The rest are small and mid-sized shops making capital decisions under very different constraints.

Walk into a typical mid-market factory, and you won’t find clean, repeatable cells. You’ll see one-off lines built around whatever equipment was affordable at the time, often run by a small team that also keeps the place from breaking.

This is where most American manufacturing actually happens. It’s also where robotics stops looking plug-and-play.

These factories don’t have automation teams. They don’t buy custom integrations. And they don’t have room for six-figure experiments that only work when an expert is on site.

As Formic’s founder, Saman Farid, put it:

“American robotics delivery has relied on expensive system integrators incentivized toward customization, cost-plus work, and lock-in. Factories get overengineered options that don’t scale.”

That complexity is manageable for large enterprises. For mid-market factories, it blocks adoption before a robot ever reaches the floor.

Less than 2 percent of U.S. manufacturing labor is meaningfully served by robotics. Not because these factories lack interest, but because the capital bar they operate under is different.

The Diagnosis Is Converging

Policymakers are beginning to describe the same problem that factories have faced for years.

∙ The Congressional Robotics Caucus was relaunched after six years

∙ 157,000 welders are nearing retirement, while most welding remains manual

∙ Most U.S. manufacturers are SMBs with no viable robotics delivery pathway

∙ Only one in ten ML engineers works on physical automationThe Real Bottleneck Is How Capital Gets Underwritten

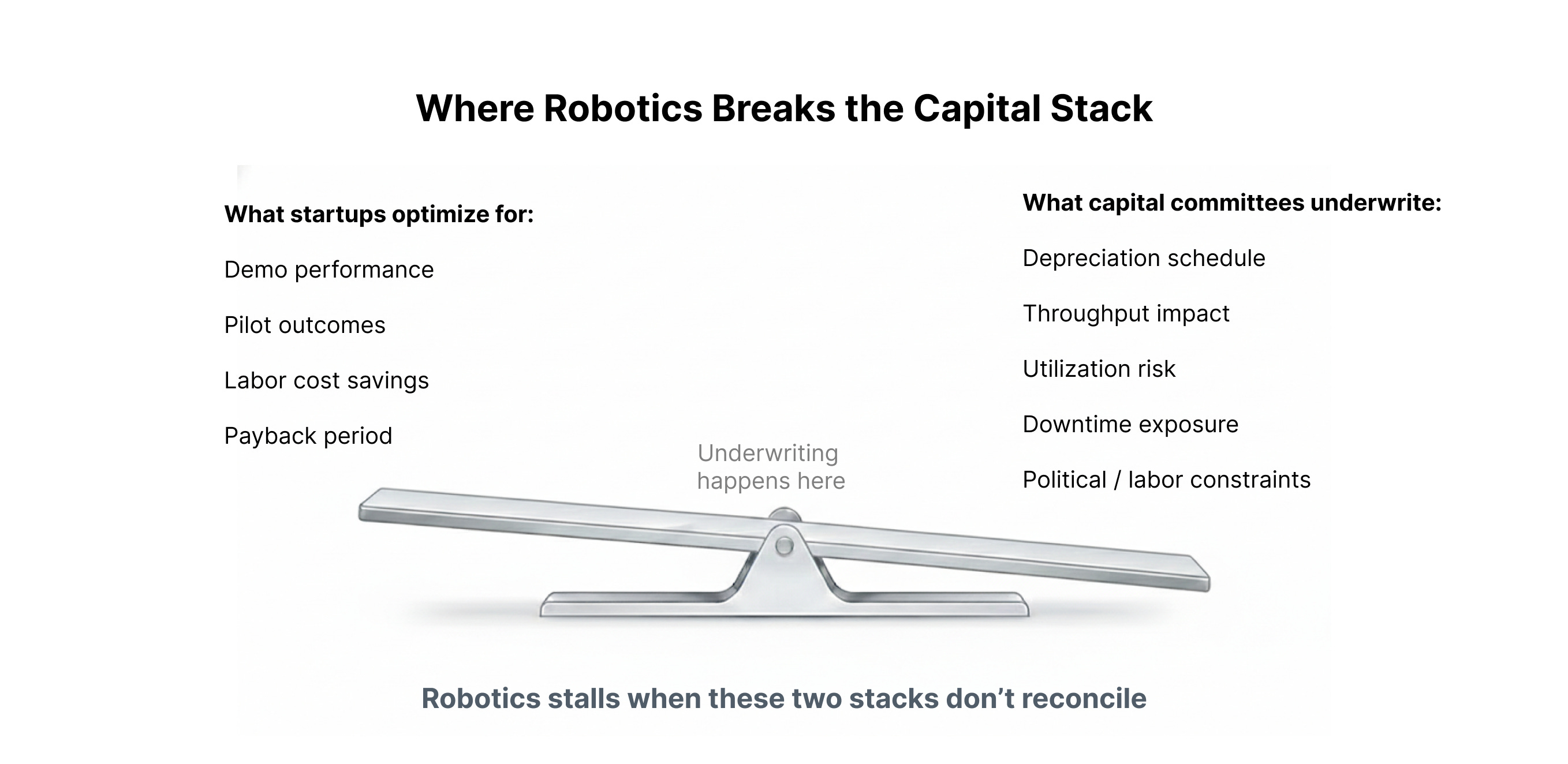

Robotics doesn’t fail because the technology breaks.

It stalls when what gets sold never lines up with what capital actually underwrites.

Most U.S. robotics is still built for a narrow buyer profile. Big factories. Big budgets. Long timelines. Teams that can absorb months of custom integration.

From the outside, robotics still looks like it’s being sold as a project. Inside manufacturing organizations, it isn’t.

Executives aren’t approving experiments. They’re underwriting production systems that have to survive depreciation cycles, labor constraints, and downtime risk.

That framing changes everything.

In large enterprises like automotive OEMs or mega-warehouses, robotics isn’t judged on demo performance. It’s judged on whether a system can fit into an existing capital plan without forcing a rewrite of everything around it.

Projects don’t survive in that environment. Systems do.

That’s why robotics tends to stall everywhere outside the top tier of buyers.

In the mid-market, automation still shows up as one-off projects. Cost-plus system integrators. Custom installs that never quite repeat. Each deployment restarts the learning curve. Lessons stay locked inside a single plant. The economics don’t get a chance to compound.

Meanwhile, the hardware keeps improving. Autonomy does too.

Deployment still stalls.

Not because the technology fails, but because the delivery model gives factories no reason to standardize, no anchor demand to plan around, and no way for learning to carry from one site to the next.

More grants won’t fix this. Bigger capex incentives won’t either.

What robotics is missing isn’t capital. It’s an operating model that lets factories underwrite automation as infrastructure, instead of relearning the same lesson on every install.

That gap is what keeps robotics from spreading across most of American manufacturing.

Where Capital Actually Decides the Fate of Robotics

When a factory leader looks at automation, they’re not asking whether the robot performs.

They’re ranking it against every other way the company can deploy capital. Build a new plant. Expand a line. Shift production geography. Or wait another year.

Robotics isn’t competing with labor. It’s competing with relocation, write-downs, and the option to wait.

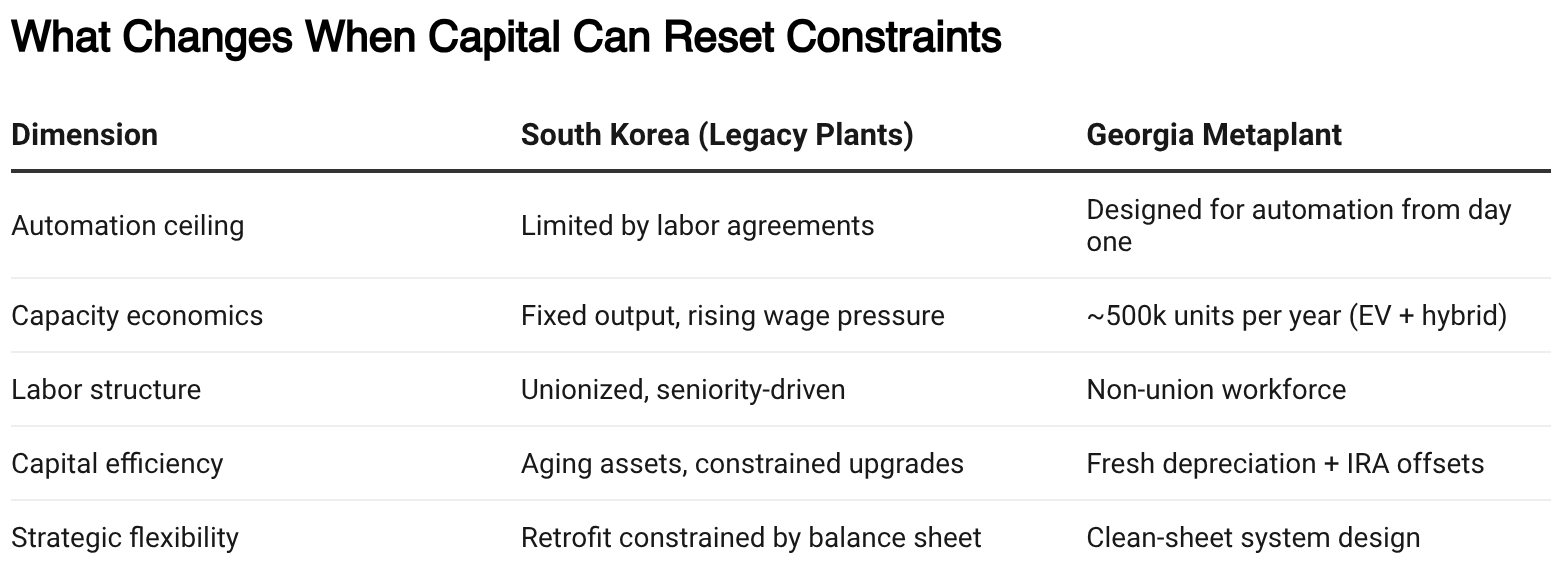

That’s why the Hyundai Georgia “Metaplant” is a useful example.

From the outside, it looks like a bet on American manufacturing. Inside the boardroom, it was a reset of the depreciation clock.

South Korea had become a high-cost, low-flexibility environment. Labor agreements constrained how automation could be deployed. Legacy lines were still on the books. Any meaningful upgrade meant fighting labor and the balance sheet at the same time.

Georgia offered a different starting point. A clean asset base. IRA tax credits. A non-union workforce. And the ability to design for automation before the first bolt was tightened.

Hyundai didn’t automate Korea harder. They removed the constraints that made automation uneconomic.

That’s the comparison every robotics startup is implicitly competing against. Not another robot vendor, but alternative ways capital can reset the system altogether.

Labor Savings Is the Wrong ROI Lens

Most robotics pitches still start with headcount. Reduce X workers. Payback in Y months.

That’s not how factories underwrite capital.

A CFO isn’t modeling labor in isolation. They’re modeling throughput, depreciation schedules, utilization, and how a system competes with every other project for capital.

A robot that technically works but sits idle isn’t a small miss. It breaks the math that the rest of the plan depends on.

One factory owner put it plainly:

“I treat robotics like any other piece of equipment. We eat the loss. But robotics is different. It depends on the software. When it underperforms, it just sits there.”

Idle automation still depreciates. It still occupies floor space. It still drags utilization below plan.

Miss a quarter, and the system stops being debated. It gets classified. A good idea. The wrong year to try again.

Once that label sticks, it rarely gets another chance in the next budget cycle.

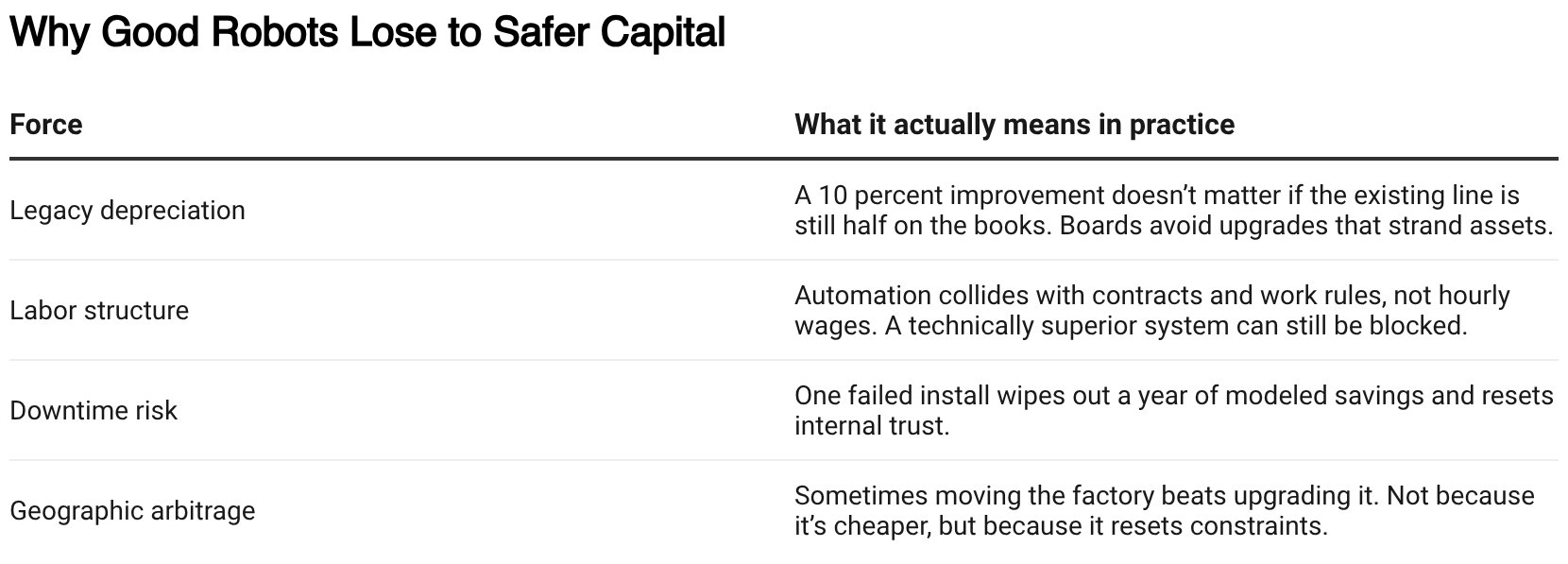

The Balance Sheet Gravity Well

From the outside, automation looks like an engineering decision. Inside a factory, it behaves like a capital gravity well.

Every robotics sale competes with forces that rarely show up in pitch decks, but dominate internal capital reviews.

None of these forces show up in demos. All of them determine whether a robot ever earns a second purchase order (“PO”).

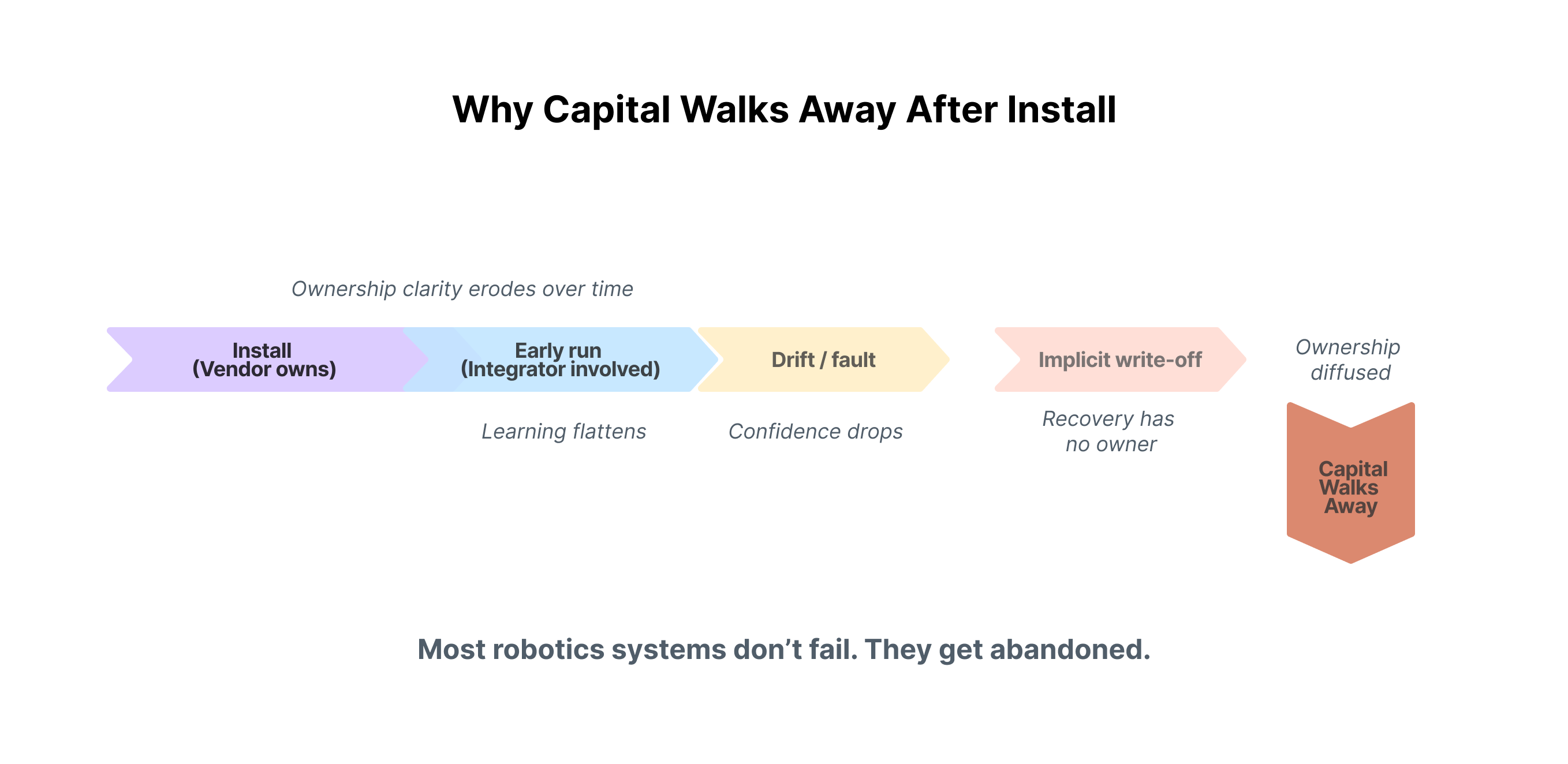

Why Robotics Dies After Install

We spoke with factory owners, operators, and engineers, including a Tesla engineer. The pattern wasn’t a technical failure. It was an ownership failure.

Responsibility evaporates once the install team leaves

When we asked who actually feels responsible six months after install, the answer was blunt.

“Vendors ship trial units cheap or free. If it underperforms, they eat the loss.”

When recovery has no owner, systems don’t fail loudly. They drift. Then they sit. Still depreciating.

What appears to be a technical stall is often a capital decision made quietly.

Learning stops once things look stable

“Once everything is working, nobody cares until things break.”

Iteration halts the moment a line runs. ROI is modeled once, then locked. There’s no budget or incentive to improve a system that already looks “good enough.”

Even basic operator tooling breaks down here. Without clean documentation and system context, AI assistants and remote support never take hold. There’s nothing durable for them to attach to.

Tribal knowledge strangles scale

“Learning breaks when documentation is weak. People protect what keeps them employed.”

“Nobody is incentivized to help integrate a robot. It feels like automating your own job.”

The second deployment doesn’t fail technically. It fails socially. Knowledge stays attached to individuals instead of moving across sites.

Repurchase is governed by trust, not specs

“If it doesn’t work on time, nobody will work with you again.”

“If I need a consultant, it’s too complex. It has to feel like buying a laptop.”

Miss a delivery window once, and the next plant goes to someone else.

Factories buy outcomes, not robots

“Companies that scale compete on cost and relationship. They support customers even when it hurts.”

“I’d pay $150k for a robot if I could trust the software like a laptop.”

This is where robotics ROI collapses. Not at install. After.

A Useful Contrast: How Failure Gets Underwritten in Mining

One contrast kept coming up in conversations with mining operators.

When an autonomous system goes down six months after deployment, someone is responsible for it.

As one autonomous mining founder put it:

“Failure underwriting depends on the business model. Operators usually take the losses. They’re money printers with tight quotas and risk-averse stakeholders. But commercial models can shift that liability by baking full-time servicing into pricing.”

That ownership changes everything.

Re-buy decisions don’t hinge on whether a system looked good at install. They hinge on how problems were handled afterward.

“Customers don’t rebuy based on what goes right,” he said. “They rebuy based on how problems are handled when things go wrong.”

Who showed up. How fast was it fixed. Whether responsibility was owned or deflected.

This is why autonomy can scale in the mining industry. Not because the technology is inherently better, but because failure is expected, priced, and dealt with.

“There’s a hidden assumption that all autonomous systems are the same,” he added. “New deployments introduce variance. The question isn’t whether variance exists. It’s whether anyone is set up to absorb it.”

Factories work differently.

Fragmentation doesn’t stop at procurement. It persists after deployment, across vendors, integrators, internal teams, and budget cycles. When something drifts, ownership of recovery stays ambiguous. Capital notices. Then it moves on.

Same machines. Similar pressure. Different outcomes. The difference isn’t capability. It’s how downside gets absorbed when things break.

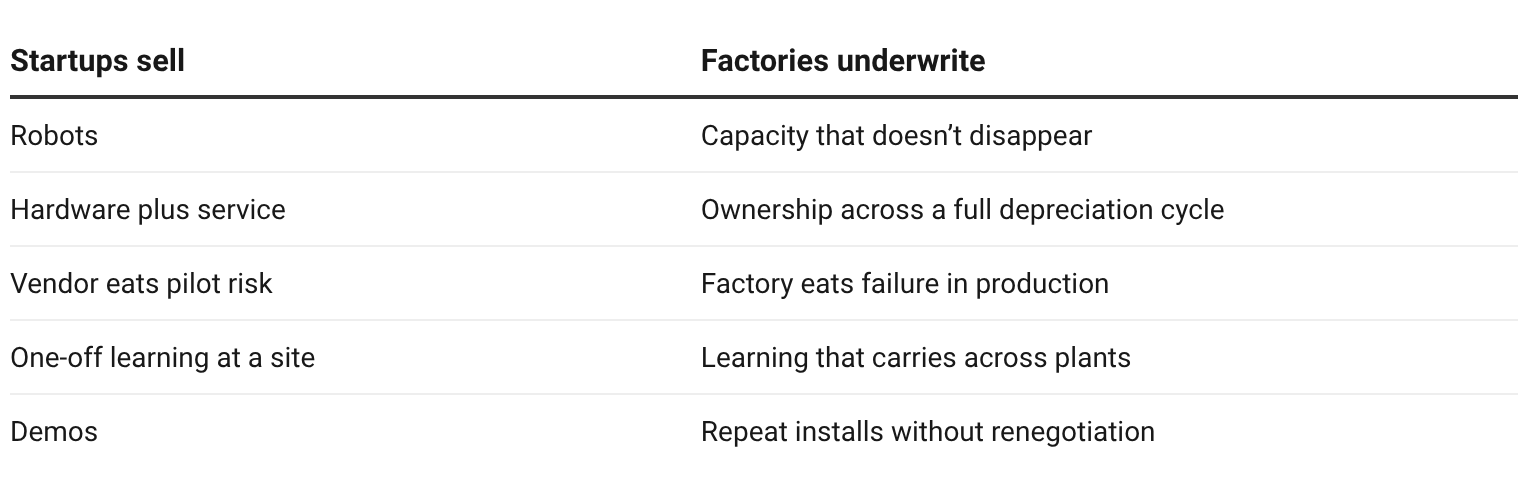

What Startups Optimize vs What Factories Underwrite

This mismatch quietly kills most robotics deployments.

Founders are rewarded for closing a sale. Factories get stuck with systems that degrade halfway through their asset life.

From the startup’s side, success is a signed PO and a demo that works. From the factory’s side, success is whether the system still delivers throughput three years later, after the integrators leave, the internal champion moves on, and the line shifts to a different product mix.

Sales teams optimize for approval. Capital committees optimize for avoiding assets that create downside.

When a pilot underperforms, the startup loses margin. When a production system underperforms, the factory eats depreciation, downtime, and internal fallout.

Those risks don’t balance. And until robotics companies design for the side that actually carries them, adoption will keep breaking at the same place: after the first install.

The Real Test of Product-Market Fit

The real question isn’t whether a startup can ship a robot. It’s whether the same factory would buy the system again without reopening the entire deal.

That second purchase is where most robotics companies disappear.

Factories don’t measure success by pilots or demos. They measure it by whether a system survives its depreciation cycle.

Does it still deliver throughput after the integration team leaves?

Does it hold up when the product mix changes?

Does it stay in use when something small breaks and no one feels responsible?

This is why robotics can look impressive on press tours and fragile on balance sheets.

A system that requires renegotiation, reintegration, or retraining every time it’s deployed isn’t a product. It’s a project. And projects don’t move smoothly through capital committees.

Until robotics is built for repeat underwriting instead of first-time approval, adoption will keep stalling. Not because the technology fails, but because it can’t clear the capital bar a second time.

The Workforce Constraint Is a Second-Order Effect

When capital stops flowing, skills stop forming.

Robotics talent doesn’t scale through certification programs or hiring pushes. It scales through repetition. Install after install. Failure after failure. Small fixes that turn into muscle memory.

When deployments don’t repeat, neither do skills.

In today’s model, most robotics projects stall after the first install. Technicians never specialize. Operators never build confidence. Documentation stays thin. Each plant becomes dependent on a handful of people who learned the system the hard way.

That’s why workforce shortages show up in nearly every robotics conversation. Not because people can’t be trained. Because there’s nowhere for training to attach once deployments stop compounding.

You can see the same pattern across industrial infrastructure. After major funding arrived, transformer lead times stretched from roughly 20 months to as long as five years, as Heather Carroll, Chief Revenue Officer at Path Robotics, observed. Capital was available. Deployable expertise wasn’t yet formed.

Roughly 157,000 skilled tradespeople are nearing retirement, while much of the critical industrial work remains manual. That knowledge isn’t disappearing because no one wants the jobs. It’s disappearing because systems don’t repeat long enough for skills to transfer.

Robotics skills form inside live deployments. During installs. During failures. During rework. Classroom training can’t substitute for that. Certifications don’t create it either.

Until robotics clears the capital bar for repeat deployment, workforce development can’t compound. Skills form inside capital-backed systems, not ahead of them.

This is why the operating model matters more than the talent pipeline. Fix delivery, and the workforce follows. Keep deployments bespoke, and every factory stays a one-off.

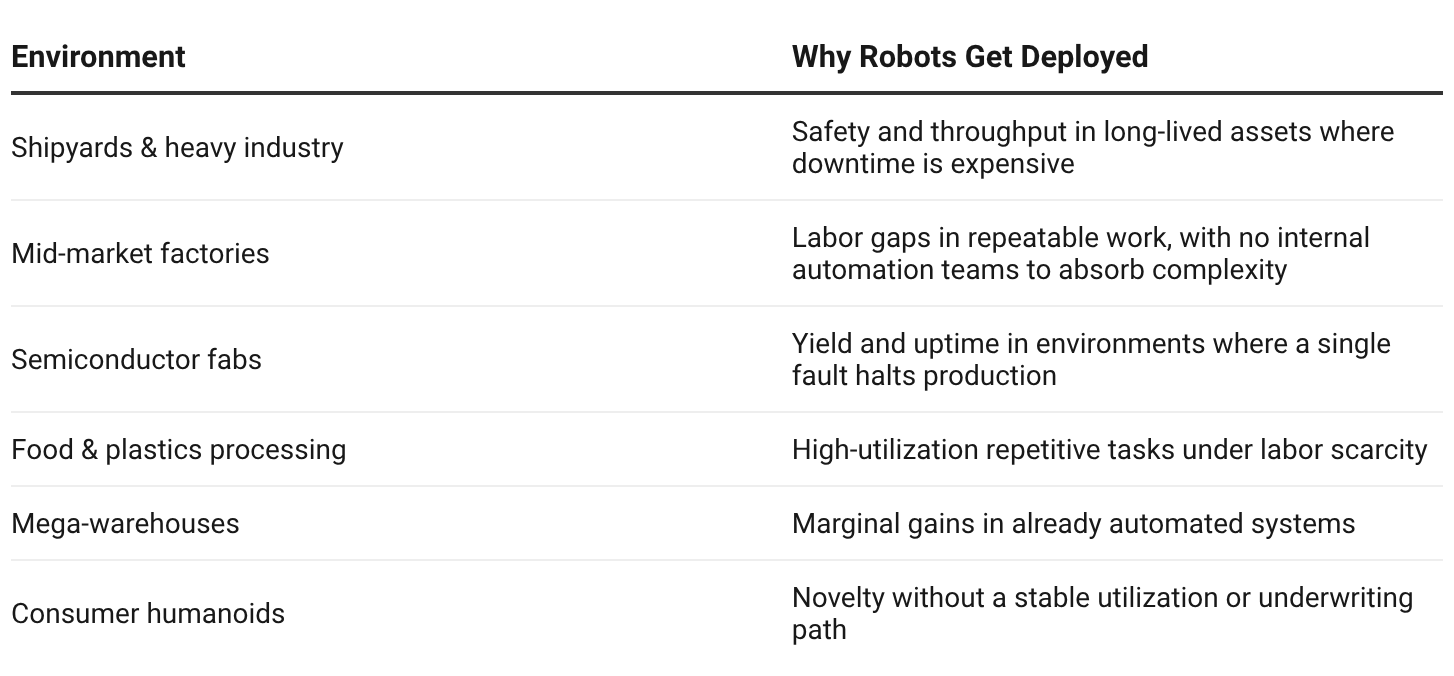

Where the Next Robotics Wave Actually Comes From

The next wave of robotics won’t come from humanoids or headline demos. It will come from places where capacity expansion is already underwritten.

These environments look different on the surface. What they share is pressure.

Uptime matters. Utilization is high. Downtime is visible.

Robotics scales when it behaves like infrastructure, not an experiment.

Automotive isn’t doubling down. Mega-warehouses are nearing saturation.

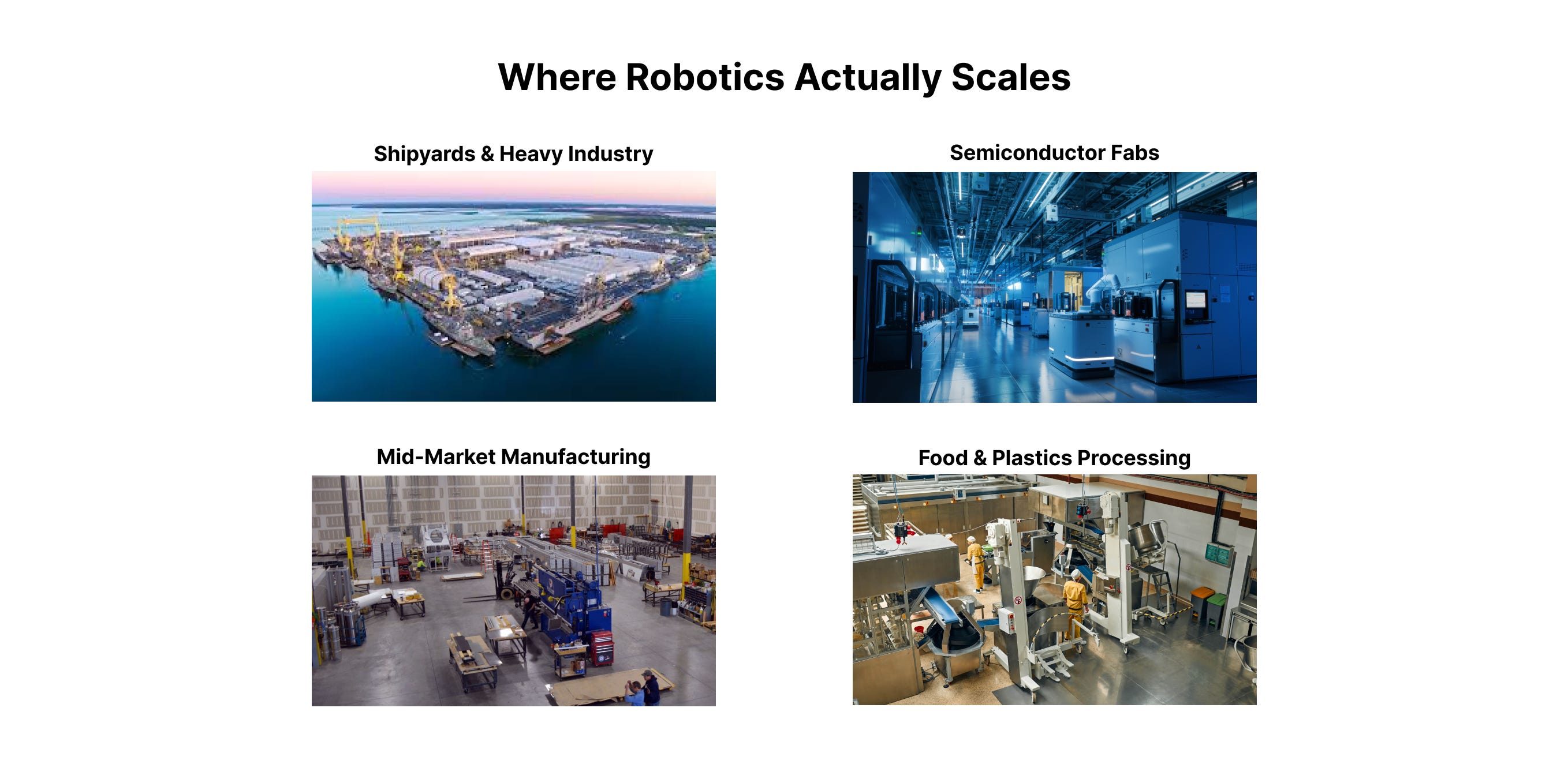

Growth is emerging in environments where uptime, throughput, and yield matter more than novelty. That includes:

Mid-market factories in metal fabrication, machining, plastics, and food processing, where labor gaps are structural

Semiconductor fabs, where downtime is existential

Shipyards and heavy industry, where assets run for decades, and labor is scarce

In December 2025, the U.S. Navy committed $448 million to modernize shipyards using robotics. Not experimental autonomy. Task-level systems. Robotic welding. Automated panel handling. Inspection.

The mandate wasn’t innovation. It was throughput at scale.

Across these environments, the mechanics repeat. Autonomy stays constrained. Utilization stays high. The economic case doesn’t rely on hope.

Take welding. A human welder might complete a few dozen meters per shift. A robotic cell can run continuously, supervised by a small team, producing several times that output. The gains only appear when parts are designed for automation. When they do, productivity compounds.

Welding. Material handling. Inspection. Surface prep. Different industries. Same economics.

This is how robotics actually scales. Quietly.

As we argued in the manufacturing essay, incumbents are often trapped by depreciation cycles. Retrofitting old plant strands capital. Real value appears when products and production systems are designed together, from the ground up.

That’s why new robotics demand clusters around greenfield capacity, constrained facilities, and long-lived assets. Not consumer demos.

You can see the pattern clearly:

The next robotics cycle won’t be led by the most impressive machines. It will be led by systems that clear capital underwriting, survive depreciation cycles, and get bought again.

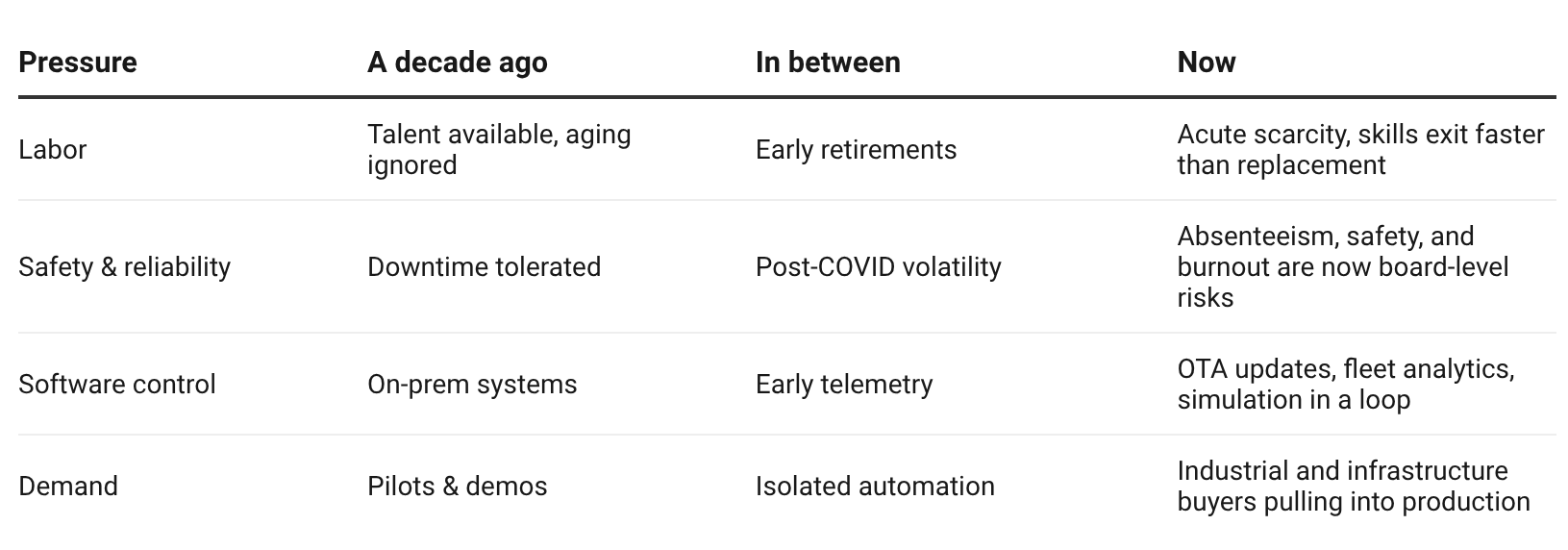

Why This Moment Is Different

Robotics didn’t stall because the technology was missing. It stalled because the pressure was optional. In most factories, waiting still worked.

That option is disappearing.

Labor scarcity has replaced labor arbitrage. Absenteeism, safety, burnout, and reliability now surface in board meetings, not HR reports. In many operations, work simply doesn’t happen without automation holding the line.

At the same time, robots finally inherit a real software control layer. Telemetry persists. Updates ship remotely. Failures can be captured, replayed, and corrected instead of rediscovered months later at the next site. Learning no longer has to reset with each install.

Demand is shifting as well. Industrial buyers and infrastructure operators are pulling automation into production. Not for demos. For throughput, uptime, and readiness.

Policy pressure is catching up. In 2025, the bipartisan Congressional Robotics Caucus was relaunched around a blunt diagnosis: reshoring won’t work without robotics and workforce alignment.

None of this excitement is new. What’s new is the cost of waiting.

Capital has fewer places to hide now. Waiting shows up as lost output. Patching strands assets. Pilots give competitors time to scale first.

Inside capital committees, the question has changed. Not whether automation is ready, but what breaks if systems aren’t redesigned around it.

Where PaperJet Plays

We’re not chasing robotics. We pay attention to where capital actually sticks.

The question for us isn’t whether a robot looks impressive. It’s whether a system survives its first real factory, then shows up somewhere else without being rebuilt from scratch or renegotiated from zero.

The teams we spend time with don’t start with autonomy slides. They start with what breaks on day three of an install. Uneven operators. Messy sites. Drift at the edges. They assume fragmentation because that’s how most factories actually run.

They build modular systems because nothing else repeats. Not because it’s elegant, but because it’s the only way learning carries forward.

Deployment isn’t treated as a handoff. It’s part of the product. If learning resets after install, the system hasn’t really shipped.

Just as importantly, these teams think early about who underwrites the first few cycles. Not as a logo, but as an operating environment. A place where failures are tolerated long enough to be fixed, documented, and reused instead of buried.

Those choices don’t show up in a demo. They show up later, when a second factory decides whether to buy the system without reopening the entire deal.

That’s usually where robotics companies either start to compound or quietly stall.

Quiet Compounding Beats Loud Demos

Demos are useful. They just don’t tell you who’s still around after five installs.

Robotics doesn’t arrive all at once. It shows up in small moments. A cell that finally holds calibration. A night shift that runs without someone hovering nearby. A factory manager who stops bracing when a fault pops up.

None of that looks impressive from the outside. Inside the plant, it changes how risk gets priced.

Each of those moments lowers friction on the balance sheet. Not because someone declared success, but because the system stopped creating surprises.

By the time anyone outside the factory notices, the decision has already been made. The system wasn’t exciting. It was reliable enough to get another budget cycle.

The winners won’t be the loudest machines on stage. They’ll look like the teams that kept showing up to dirty floors and boring problems long enough for the economics to start repeating.

The Question That Matters

If this essay resonated, it’s usually because you’ve seen some version of this failure up close.

On a board. In a plant. Inside an investment committee.

The question isn’t whether robotics works.

It’s how systems get underwritten, so learning compounds instead of resetting.

That’s the conversation worth having.

Thanks for reading.

Best,

Chris Kong

Founder & GP, PaperJet Ventures

P.S. A sincere thank you to Jen Liao, Lawrence Wong, Bola Adegbulu, Ellen Chang, Johann Dias, Jisoo Chung, and Jaireh Tecarro for the thoughtful feedback and perspective shifts that helped sharpen this piece.

Awesome Chris! So much to chew on here. The opportunity in mid market is huge, great to understand the contraints and points of failure. Sharing!

Great read! Thanks for sharing, Chris!